Unlocking ETH

Ethereum just turned 10. A full decade of innovation, billions secured, and zero downtime.

If you believe in ETH for the long run, ask yourself: Is your ETH working for you?

This post breaks down 3 simple ways to earn more ETH. Not by flipping tokens, but with real yield. Let’s start with the basics.

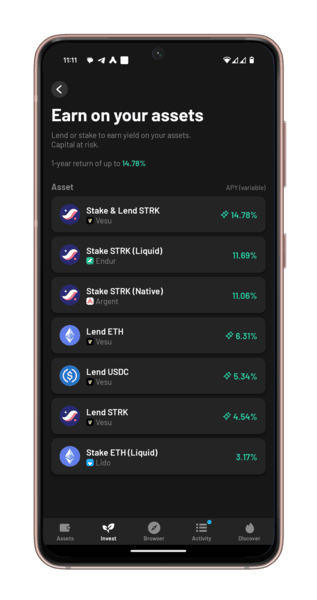

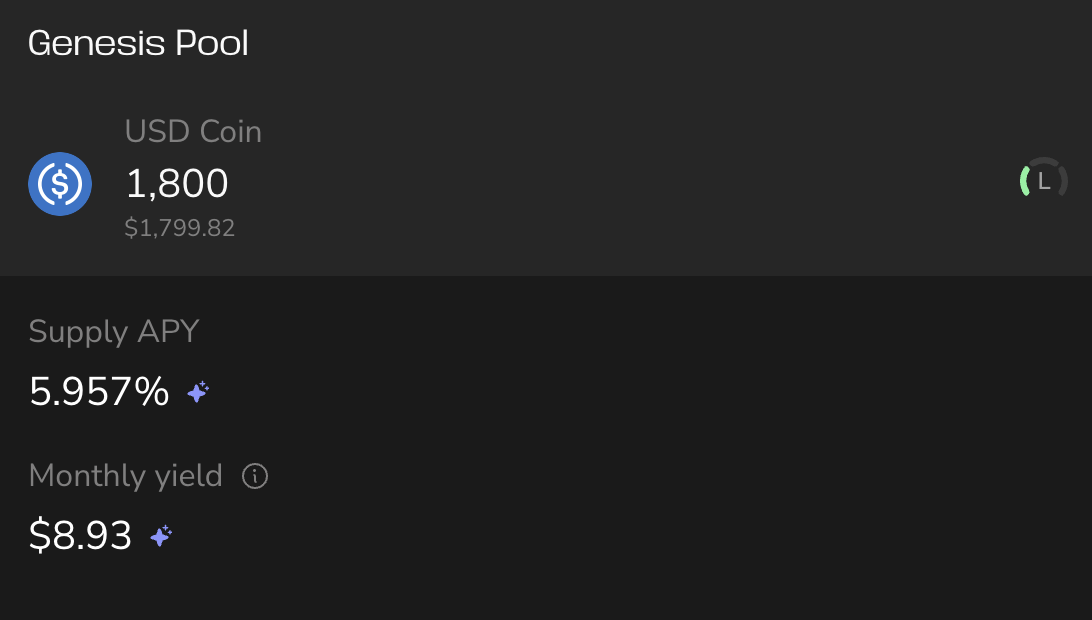

Level 1: Simple lending

Basic yield, zero stress

If you want passive yield with minimal setup: supply ETH or wstETH to a Vesu pool.

You earn lending yield and DeFi Spring rewards. wstETH also earns staking rewards on top.

Current rates are around 4%, and go higher when markets heat up.

Risk: Like all lending platforms, there are smart contract, oracle, and pool config risks. Vesu reduces these with audits and known curators.

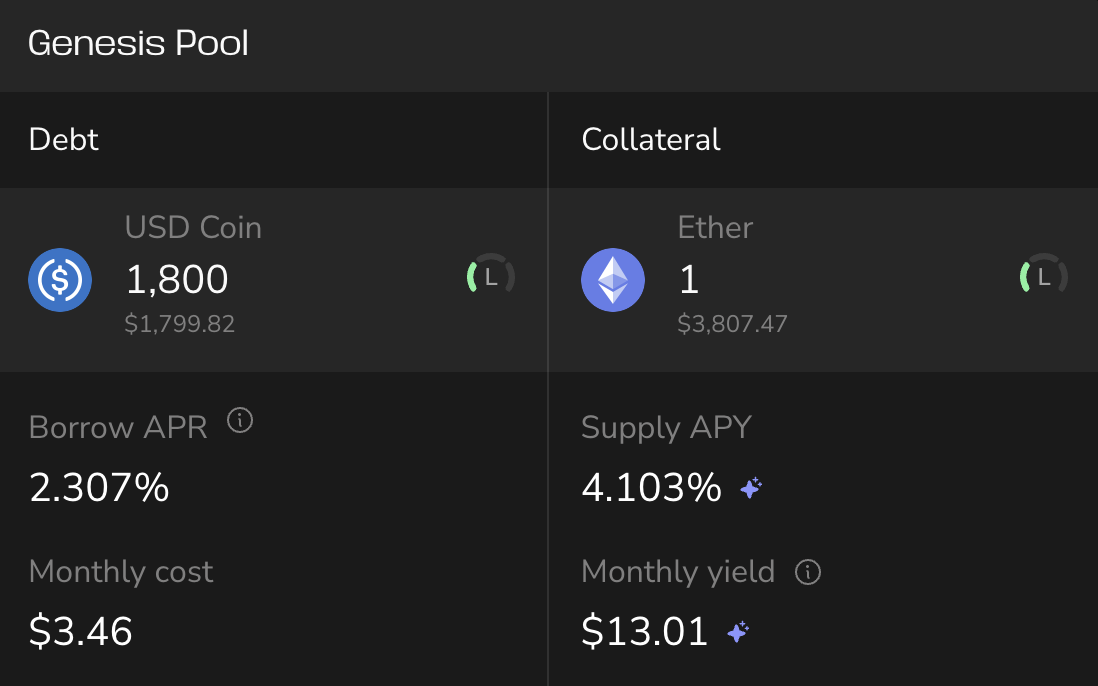

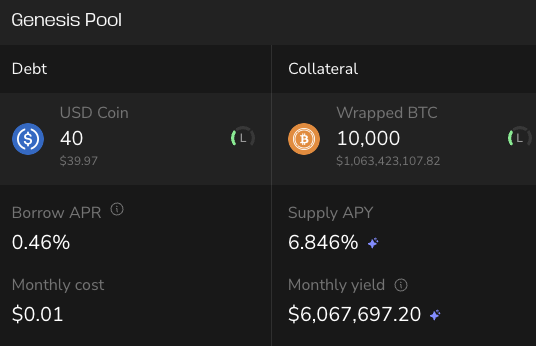

Level 2: Lending & Borrowing

Double the yield

Deposit ETH or wstETH, then borrow stablecoins like USDC or USDT.

You can then deposit those stables into another Vesu pool to earn some extra yield.

Right now, you earn around 4% on your ETH, and 5–6% on the borrowed USDC. Your ETH keeps earning, while the borrowed stables generate yield on top.

Risk: Same as Level 1, plus exposure to ETH price drops. If ETH falls too much, your position can be liquidated. Start with low borrow amounts and monitor your loan-to-value ratio.

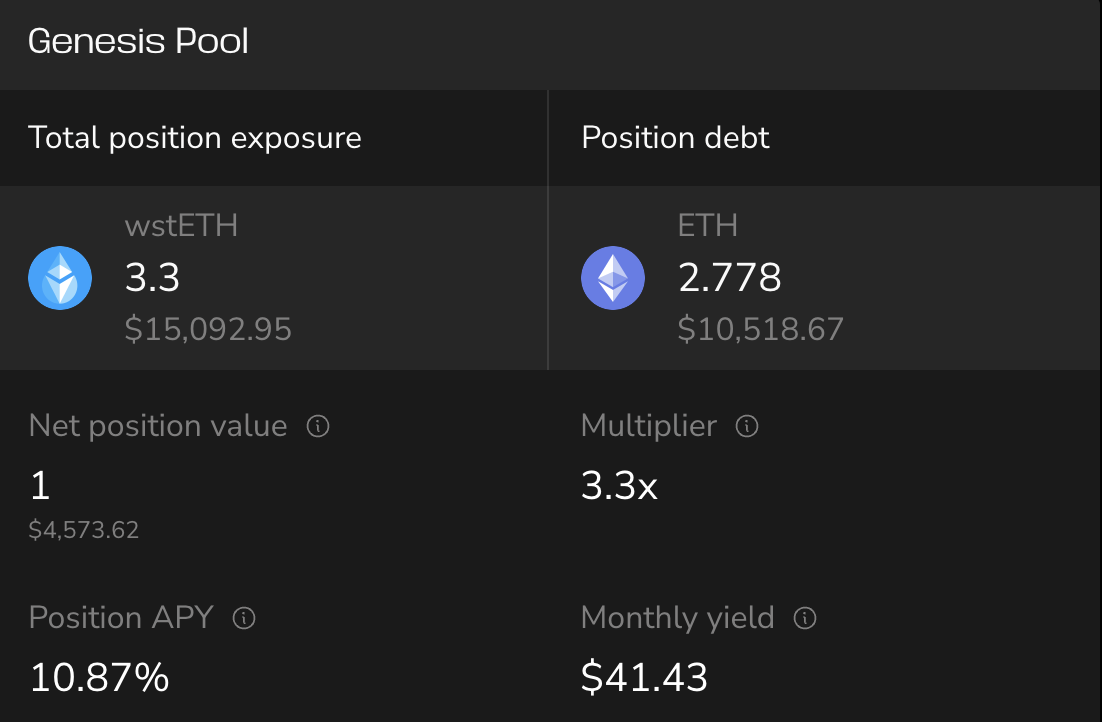

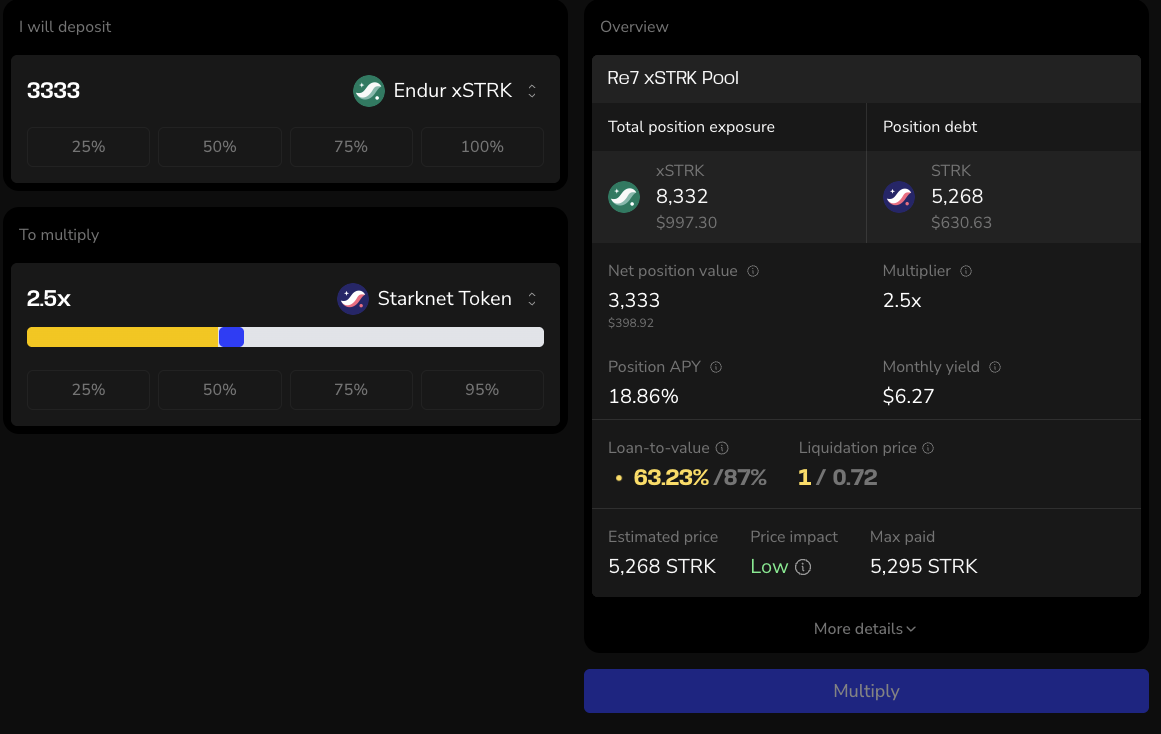

Level 3: Multiply it

More exposure, more yield

Multiply lets you increase your exposure to Ethereum.

You supply wstETH, borrow ETH, and use it to buy more wstETH. All in one transaction.

Current examples show around 10% APY with a 3x multiplier. You can pick your own level, but higher yield comes with more risk.

Risk: ETH and wstETH prices are correlated, but extreme market stress can break that link. If prices decouple too much, your position could be at risk of liquidation. Learn more about Multiply in our Docs and choose a multiplier that fits your risk tolerance.

Make your ETH work

Three levels, one goal: earn more ETH

Whether you’re lending, borrowing, or multiplying, Vesu's got you.

Explore the strategies, choose what fits, and grow your stack.

Got questions or feedback? Come hang in Discord. Check out the Docs if you want to dig deeper.

Ethereum isn’t slowing down. Neither should your yield.

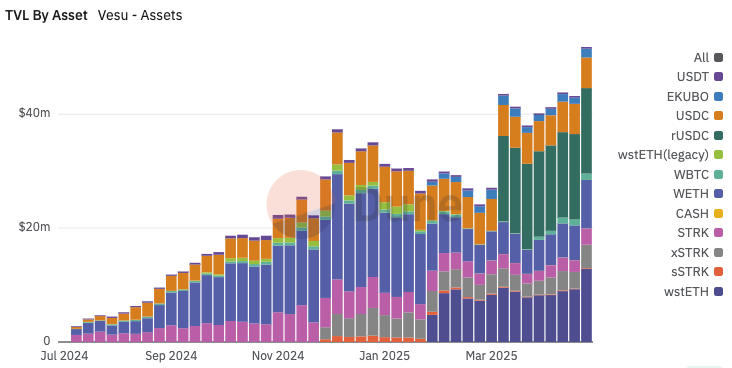

Vesu TVL breakdown by asset, as shown on Dune.

Vesu TVL breakdown by asset, as shown on Dune.